BUDGETARY CONTROL – AN OVERVIEW:

Budgetary control is basically planned to assist the management in allocation of authority as well as responsibility to aid in making estimates or plans as far ahead as possible, assist the comparison of actual performance with the budgeted estimates and to take suitable remedial actions to remove any deviation in the performance so, that the desired organizational objectives can be achieved.

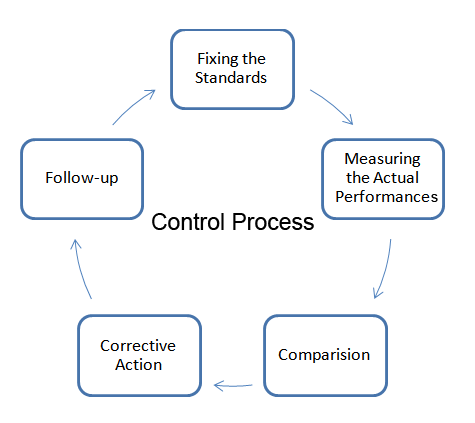

The budgetary control is a continuous process which helps in both the planning and controlling. A budget is a means and budgetary control is the end-result. The essentials of budgetary control include:

- Establishment of budgets for each section of organization

- Executive responsibility to perform specific task

- Comparing actual and budgeted figures to know the variations

- Placing responsibility for such failure to achieve desired results

- Taking suitable remedial action

- Revising budget in light of changes followed

The Chartered Institute of Management Accountants, London, defines budgetary control “as the establishment of budgets relating to the responsibilities of executives to the requirements of a policy and the continuous comparison of actual with budgeted results either to secure by individual action the objective of that policy or to provide a basis for its revision”.

BUDGET, BUDGETING & BUDGETARY CONTROL:

- Budgets are the individual objective of department either in terms of rupees or quantities against which the actual performance is measured.

- Budgeting may be defined as process of preparing budgets.

- Budgetary control involves the utilization of such budgets as an important management tool for business planning and controlling.

PRELIMINARIES OR STEPS OF SOUND SYSTEM OF BUDGETARY CONTROL:

Following are the important steps or preliminaries for effective implementation of budgetary control system:

- The organization must have organizational chart to get a clear view of authority and responsibility of each executive.

- The objectives and policies of business should be clearly defined and stated.

- The budgeted output should consist of clear terms.

- There should be an effective system of accounting to record necessary information.

- Budget committee should be set up.

- There should be a proper system of communication between various levels of management.

- Budget centers should be established.

- There should be budget manuals.

- The budget should cover all the phases of an organization.

- It is important to get top management’s approval.

ADVANTAGES OF BUDGETARY CONTROL:

The advantages of budgetary control can be summed up as follows:

- Conducting business in most efficient manner: It allows the management to conduct business in efficient manner as the budgets are prepared to ensure that all the resources should be put to efficient use and the organizational objective can be achieved with efficiency.

- Management by exception: Budgetary control has made the management by exception possible as the comparison of actual and budgeted figures will point the inefficiencies and the remedial action can be taken to remove those differences in performances.

- Lays emphasis on staff organization: Budgetary control also ensures that executive responsibility for each function of business is clearly defined and required authority to fulfill those responsibilities must also be delegated.

- Effective utilization of four M’s: Budgetary control allows the production process by taking into view the available quantity of four M’s such as men. Money, material and machinery.

- Performance of various functions of management: Functions of management such as planning, controlling and coordinating can be performed well under budgetary control.

- Cost consciousness: It also helps in bringing the feeling of less wastage and reduced expenditure within the organization and also The expenditure beyond the budgeted figures requires the permission of higher authority.

- Reviewing changing trends: It also allows the organization to make changes in the budget in light of changing trends in terms of technology or customers tastes etc.

LIMITATIONS OF BUDGETARY CONTROL:

Budgetary control as a tool of management has the following limitations:

- Rapidly changing circumstances: Although the budgets can be and has to be revised from time to time in light of changing circumstances but frequent revisions may prove to be costly.

- Coordinating budgets of various functions: Small organizations cannot afford this tool of management as it is quite costly to correlate or coordinate the budgets of different sections of organization.

- Conflicts among various functions: Various sections in organization will try to get more share of allocated resources, shirk responsibility hence leads to conflicts.

- Impossible to achieve budgeted targets: Future being unpredictable, the future forecasts and estimates can never be accurate. hence, the question of achieving them all does not arise.

- Not a management substitute : Budgetary control is quite an important tool of management but cannot be treated as a substitute of it.

Leave A Comment